How to Travel Hack with Free Trips the Smart Way!

Apr 27, 2025

Kyle and I got married in December 2011. I had one credit card and he had none. I started using my credit card for all our expenses and paying it in full once a month - despite both being college students and having 2 part time jobs that each paid biweekly. To say money was tight would be an understatement.

A few months into our marriage, I messed up the timing of the monthly payment and was charged interest. I remember it being less than $50 but I still cried: because I had never paid interest before and because we could not afford any expense beyond our small, necessary, set expenses.

I decided to do away with using a credit card altogether and exclusively use the debit card so that I couldn’t buy things I didn’t have money for and I couldn’t mess up a payment.

In the summer of 2012, I saved up enough to pay off our previous month’s credit card bill and start putting all our new charges on the debit card.

From the summer of 2012 until the fall of 2021 I did not use a credit card. During those 9 years, we paid off $26,000 in debt, saved a full emergency fund, had 4 kids, bought our first home, and launched Debt Free Mom.

In 2021, Kyle and I both turned 30 and we celebrated our 10th wedding anniversary (yes, the math on that is correct. We got married at 20.)

We had 4 kids within 6 years and knew our family was complete.

We were ready to celebrate and take a big trip. There was only one problem. We did not have the discretionary income to afford a big trip.

Enter responsible travel hacking. I had followed Aunt Kara on instagram for a while simply because I appreciated her approach to finances and was curious about her travel hacking methods. But I was in the shadows, not actively engaging or opening cards.

I asked myself: “could I manage this responsibly? Do I have the track record and time to start using credit cards in a way that is beneficial instead of harmful?”

I decided the answer was yes - only on a trial basis. I decided to travel hack for this big anniversary/birthday trip and then give myself permission to stop if it was too complicated, involved, or tempting.

We spent 8 absolutely amazing days in Puerto Rico - and covered over half of our $3,500 Airbnb as well as almost all of our $600 in flights using credit card points from Chase Sapphire Preferred and Southwest Rapids Rewards cards.

So with how amazing and inexpensive that trip was, do I regret going 9 years without doing this?

Why 9 years without credit cards was best for me:

- The long-term success of my finances and my relationship with money desperately needed a time in my life when I paid in cash, only bought things when the money was already in my account, and didn't even have the temptation to swipe and figure it out later.

- While these rewards are amazing and can cover or offset the cost of the big things like transportation and lodging, they don't cover any of the spending purchases, food, gas, etc. I would have still needed disposable income for the other parts of the trip - and for a while, I simply didn’t have it.

So while I am all about travel hacking now, what I learned in those 9 years made it possible for me to enjoy the benefits of responsible travel hacking without the pitfalls.

Before I share the specific cards I have and how I earn points with them, here is the “am I ready for this?” checklist I used to evaluate myself :

- Have I demonstrated that credit cards are not a temptation to overspend or swipe mindlessly? If you currently have debts with high interest rates that you’re slowly trying to pay off and being charged interest, now is not the time to open new credit cards. If you have a history of maxing out cards and then slowly paying them off, travel hacking may not be for you. If you’re focused on reducing your debt minimum payments and using your paychecks to pay for your future instead of your fast for the very first time, your season of travel hacking may be a little ways down the road. And that’s ok! Remember, you’re hearing this from someone who didn’t use credit card rewards at all from the age of 21 to 30 - and whose finances were better because of it.

- Do I have an emergency fund of at least one month worth of expenses to protect you from the unexpected both at home and while travelling? It’s a fact that when you travel to unfamiliar places, your likelihood of unexpected expenses goes up. Car breakdowns, accidents from adventures, miscommunications from language barriers, and complications with arriving or leaving all make it even more likely for costs you didn’t plan for than you have at home.

If you are planning a vacation and can only afford the vacation if nothing goes wrong, you can’t afford the vacation. - Do I have a track record for planning my spending in advance (aka a budget) and then following through with tracking your spending (aka using the budget?)

Travelling responsibly includes planning to the best of the knowledge you have available how much the trip will cost in total - not just the easy to calculate costs like flights and hotels. I want to see a track record of planning how much you’d like to spend, adding a budget buffer to this plan, and then sticking to the plan as much as is in your power. If your default travel approach is to just swipe, swipe, swipe, and pay off the balance when you get home “because it’s vacation!”, adding travel hacking credit cards to your life is a dangerous game. - Are you willing to commit to taking breaks from the credit cards anytime your finances feel messy? I'll be honest: having a budget and exclusively using a debit card is WAY easier than monitoring multiple credit cards on top of your bank account and budget. There’s just no way around that. When the only things I monitored were my one checking account and my budget, it was quicker, more accurate, and easier to stay consistent with.

You need to view the additional work and administrative effort involved in travel hacking like a part time job. You do more work than you did before and in exchange you receive travel funds you didn’t have before. The rewards are not free - they cost your time, effort, and discipline. - Do you understand the basic mechanics of credit cards and their rewards? For example, carrying a balance does NOT earn you more rewards than paying the card all the way off at least once a month if not more frequently. I have always paid my card in full down to $0 at the end of every pay period twice per month. I do not even know what my statement balances are because I do not pay the card according to that cycle. I start each pay period with a $0 balance (minus pending charges), budget for every single new transaction during the pay period, then pay the card down to $0 again at the end of that pay period.

I have always done it this way and have always earned exactly the same amount of rewards that someone who carries a balance or who pays the statement balance a month later does.

The moment you pay any interest (generally 20-28%) on a card that is only paying you 2% cashback, you’ve lost every benefit or reward. These rewards are only truly rewards if you never pay interest. If at any point you find yourself carrying a balance but keeping the card for the rewards, it’s time to take a step back and evaluate priorities and spending habits. For example, if your card has 20% interest and 2% cashback, you’re being charged 10 times more than you’re earning. You’re losing money on that card, not gaining a single penny.

My Current Credit Card Strategy:

- While earning points on everyday purchases can slowly add up over time, the large bonuses that allow us to fully cover flights or hotels will almost always come from the combination of earning sign on bonuses and referring each other to new cards. It is this revolving door of new offers that earns enough for a week on the beach, not earning $30-40 per month when I shop.

- Open 1-2 new cards per year and close the same number. I need to get better at closing cards but we are currently in the mortgage process. I closed one card in January and now I’m not doing anything until we close on a future house. When I closed a card in January, my score went down around 10-15 points and in the last months has come back up almost all the way to where it was before.

If you simply google something like “how often can I earn the Chase Sapphire preferred sign on bonus?” you’ll get the most up to date rules on how frequently you can sign back up and earn the same thing you’ve earned before. Chase Sapphire is currently 48 months and Southwest Rapid Rewards Card is every 24 months. The Capital One repeat bonus is more vague and not posted on their site, but I found multiple reddit users posting they successfully received another bonus 48 months apart. - Keep a record in my budget of which cards earn the most rewards in each category. I only pay attention to this when I’m not actively trying to fulfill a sign on bonus. If I’m working towards a sign on bonus, all expenses go on that card regardless of category.

- When I open a new card to earn the sign on bonus, I take 30-45 minutes to log into all my online bills and add the new card as the payment method. Again, this is the work involved in earning the rewards. They aren’t free and they take time and administrative effort, but they can be worth it!

- Always use a referral link from one spouse when opening a new card for the other. This is one of the biggest ways to earn points if you are in a two-adult household. Each person can earn sign-on bonuses from opening their own card (even if they are the same kind of card) and on top of that, spouses can refer each other to the new card and earn a bonus for it. I don’t make us authorized users on each other’s cards because I don’t need to. But you can do that and still open a card in the other person’s name and earn a referral bonus for it. Having an authorized user card does not count as having an account.

- Close cards only when they’ve been open more than a year - never close my oldest card or Kyle’s oldest card. I learned this from Aunt Kara: you can disqualify yourself from earning future bonuses or being approved for future cards with that bank if you close a card less than a year after opening them. Essentially, be willing to pay the annual fee twice: once at time of opening and again at first renewal before closing the card.

- Keep a spreadsheet of all important details: when I open cards, when I earn the sign on bonus, and when the annual fee is charged. Add these fees to my budget and only delete them if the card is closed.

- I also occasionally check in to make sure the benefits I receive meet or exceed the annual fee of the card. For example, the Chase Sapphire Preferred card gives me one $50 hotel credit per year, a 10% anniversary bonus (I usually get around $15), a DoorDash Plus membership (I only use it occasionally, but it’s nice!), and 5x points back on travel booked in the chase portal (equivalent to 6.25% cashback - higher than any other card!).

- Those things added together roughly equal the $95 annual fee. Which means the normal points I earn on that card throughout the year (typically $50-60 per month) are truly extra money and not just offsetting the annual fee.

- Use my budget to determine how realistically I can complete the sign-on bonus for a card and only opening a new card when I know I’ll meet the sign on bonus (often I do this close to a large purchase or big trip). This means being willing to let increased offers or bonuses pass or paying for trips without travel hacking if I don’t clearly see in my budget how I’ll fulfill the sign on bonus. This is the tightrope we walk: earning travel wisely. Enjoying the benefits because we say no when the benefits are going to be overshadowed by overspending or unmet bonuses.

I know reading this list will naturally lead to more questions. My suggestion to you is this: start as small as possible. One card. One sign on bonus. Redeem it for one travel expense. Taking these actions will allow you to build up to as complex or as simple of a strategy as you would like to have.

Having me answer every possible contingency for “what about this?” before you’ve even opened a card won’t help a ton only because my answer will naturally lead to another question - to infinity. Until you’ve actually opened an account and see with your own eyes that it works.

What Happens When You Open Your First Card

- You apply to a card using your social security number and basic income information in order to be approved. Remember, this is truly opening a loan. You receive a line of credit and agree to the repayment terms and the interest charges if your card is not paid in full each month. I have never had my credit score go down more than 2-3 points by applying to a card.

- When you are approved, the clock starts ticking on your sign on bonuses. For example, if you have to spend $4,000 in 3 months, it will be 3 months from the day you were approved for the card. You will also be charged for the annual fee on the card right away unless the card specifically offers no annual fee for the first year (I’ve never had this on the cards I have). Be prepared in your budget to pay for whatever the fee is on the new card in the very first billing cycle.

- You’ll receive your card in the mail in a few business days. Start using it right away and change any auto-pays to this new card.

- Most of the cards I use are managed through Chase and then I have one card type through Capital One. Both of these banks have a visual tracker inside your online account to show you how much you’ve spent towards the bonus goal. You won’t have to track it personally or keep a record. When you login, you’ll see how far along you are in the process.

- You do not earn the sign-on bonus or any rewards based on the balance on the card. I repeat, you do not have to have a BALANCE of $4,000 at one time on the card in order to earn the bonus. Every spend requirement and every reward point earned is based only on your actual charges: no matter how quickly you pay them off. You could pay your card off completely at the end of every DAY and as long as you had $4,000 of charges in 3 months you would earn the sign on bonus.

- Chase and Capital One handle things slightly differently when it comes to your rewards becoming available: Chase only makes rewards available once a month at the statement close date. This includes the sign on bonus. For example, if your statement closes on the 10th of every month and you complete the spend requirement for your card on the 20th of the month, you won’t receive access to the bonus until the statement closes on the 10th of the next month. You’ll see the bonus pending in your rewards within a couple days of achieving the requirement, but you won’t be able to use it until it actually posts to your account. This also applies to referral rewards. If you refer someone in the middle of a spending cycle, you’ll receive access to your referral bonus when your statement cycle closes.

Capital One gives you access to your standard rewards and sign on bonuses as soon as you earn them. When I spend on the card, as soon as my transactions are posted, the rewards I earn for them become available. (2x miles which is equivalent to 2% cashback). This applies to referral bonuses as well. They are available to use as soon as you’ve earned them. - Choose your first travel redemption and give it a try! The very first time I ever redeemed rewards I was so nervous. 😅 I was convinced it would somehow decline me or I’d show up to the hotel and they’d say “we have no record of you!” So I played it really safe. I used a small part of my very first sign-on bonus to book a one-night hotel stay in St. Louis about 2.5 hours away from home. We did a zoo day then spent one night in an Embassy Suites and drove home the next morning! First free hotel night: ✅

This gave me the confidence to understand how the portals worked (I booked this hotel inside the Chase Travel Portal) and confirm that I do in fact have rewards and they do in fact work. I’m a major skeptic about new and unfamiliar things. - Keep a slow-and-steady approach. Opening 7 cards at the same time and failing to meet the sign-on bonus simply means you’re on the hook for 7 annual fees without any rewards. I opened two Chase Sapphire preferred cards and One Southwest card in the fall of 2021 for our Puerto Rico Trip. Then I didn’t open any others for at least 6 months. I needed time to understand them and accustom myself to the budgeting changes and paying them down to $0 every pay period. Remember, I had been exclusively using a debit card only for 9 years: this was a big change!

Exactly Which Cards I Have in the Order I Opened Them

[this post includes affiliate links]

Chase Sapphire Preferred

I opened this card in the fall of 2021 when we were planning our anniversary trip to Puerto Rico. After we met my sign on bonus (spend $4,000 in 3 months - $1,334 per month) we then opened the same card for Kyle and earned the sign on bonus a second time. This gave us points worth over $2,000 when used in the Chase Portal redeemed for travel and paid for a few hotel nights in local hotels and then half of our Airbnb in Puerto Rico!

A limited time offer (as of 4/24/25): Chase Sapphire Preferred Sign on Bonus is currently 100,000 bonus points after you spend $5,000 in the first 3 months. Points are worth 1 penny UNLESS they are used to book travel inside the Chase Portal then they are worth 1.25x. This means this sign on bonus would give you a reward with $1,250 in Chase Travel! 😱 This is the highest offer they run. The standard sign on offer is 60,000 points which is equivalent to $750 in Chase Travel.

Standard Earnings: 5x points on travel booked within the Chase Portal and paid for with the credit card instead of points, 3x points on restaurants, 2x points on travel purchases not booked in the travel portal, 1x points on everything else.

Current Referral Bonus: 10,000 points for the person who referred a friend.

Annual Fee: $95

Other highlights of this card: An annual $50 hotel credit (pay for a hotel through the portal on the card at any point during the year, get a $50 statement credit at annual cycle close once per year), Free DoorDash Plus Membership

Cons: less versatile redemption options than Capital One (can’t redeem points for things like Airbnb at the higher 1.25x rate). Points only become available once per billing cycle.

Sign Up Here for Chase Sapphire Preferred

Southwest Rapid Rewards

This is a much simpler card both in earning and redeeming points for me. I opened it for the sign-on bonus and a temporary offer where I could receive the Companion Pass good for one year. The Companion pass allows one person to fly for free with the card holder. It truly works, we use it all thet time, and it’s crazy beneficial!

It’s managed by Chase so it will be a Chase account you log into.

You earn Rapid Rewards for purchases as well as additional points for flights (the same way you can earn rapid rewards points through Southwest without having a credit card). These points can be used to cover flights when purchasing on the Southwest website.

Current Sign on Bonus as of Jan. 2023: 50,000 points after spending $1,000 in the first 3 months. Much lower spend requirement! 50,000 points can be worth over $500 depending on the flights booked.

Current Referral Bonus: 20,000 points for the person who referred a friend.

Annual Fee: $69

Perks: 2 earlybird check-ins per year! 2x points for every $1 spent at Southwest, 2x points on local transit/commuting/ridesharing, 2x points on internet/cable/streaming, and 1x points on everything else. 3,000 bonus points at each anniversary renewal. With Southwest changing their bag rule starting this summer, if you book flights using a southwest credit card, each person on the itinerary (up to 8 people) can fly with one checked bag free.

Sign Up Here for Southwest Rapid Rewards

Capital One Venture Card

I opened this card in October 2022 - almost a full year after I had opened any other card. We were planning a trip to Colorado to visit family. I had covered all our flights using the Southwest rapid rewards card and was looking to earn a sign on bonus in order to cover a minivan rental for 5 days.

At the time I signed up, the bonus was (and still is) 75,000 bonus miles after spending $4,000 in the first 3 months.

This can be used to book travel directly in their capital one portal (this is how I booked our NYC trip). It can also be used to cover eligible travel purchases. Any purchase that gets categorized as Travel can use miles to reimburse yourself for that purchase (this is how I covered a hotel stay in Colorado when we needed to stay close to the airport last minute due to a snowstorm. I paid for the hotel, then when I got home used points to get a statement credit back).

Sign on Bonus: Limited Time Increased Offer: 100,000 miles when you spend $5,000 in the first 3 months. This is almost always 75,000 miles - I’ve never seen it this high! This is equivalent to $1,000 in travel that can be used inside the Capital One portal for things like flights, hotels, or rental cars. It can also be used for Airbnb! You pay for the Airbnb using the credit card, then cover the purchase with your available miles and you receive a statement credit. I’ve done this many times!

Standard Earnings: 2x miles on every purchase (equivalent to 2%. For example, you’ll earn 200 miles on a $100 purchase and those 200 miles can be redeemed for $2.)

5x miles on travel booked inside the Capital One Travel Portal.

Referral Bonus: 10,000 miles earned for the person who refers a friend

Perks: This is the most versatile card for redeeming points. You can buy anything coded as travel with the credit card and then use your points to cover the purchase by receiving a statement credit. As mentioned above, you also have access to your miles as soon as they are earned.

Annual Fee: $95

Sign up for the Capital One Venture Card here

Chase Ink Business Cash

This is my newest card! You don’t have to have a business filed as an LLC. You can sign up with your SSN if you have side hustle income or self-employed income like contract work of any kind.

Annual Fee: $0 - the only one I have with no annual fee!

Current Sign on Bonus: $350 bonus when you spend $3,000 in the first 3 months and another $400 if you spend $6000 total in the first 6 months!

Referral Bonus: 20,000 points ($200) if you refer someone

Perks: 5% cashback on purchases at office supplies stores, internet, cell phone, and cable services. Aunt Kara taught me to buy gift cards at office supplies stores! 2% cashback on gas and restaurants (max of $25,000 spend per year), and 1% cashback on everything else.

These points are only a 1:1 redemption rate, however if you have a Chase Sapphire Preferred card, you can easily transfer your Business Ink points to the CSP card and then redeem the for travel as described above with a 1.25x redemption rate which is what I always do!

Kyle and I each have this card. I use one of them for personal expenses and one of them is my business credit card for all business expenses. No annual fee so I don’t worry about closing and re-opening unless I am eligible to earn the sign on bonus again.

Sign up for the Chase Ink Business Card here

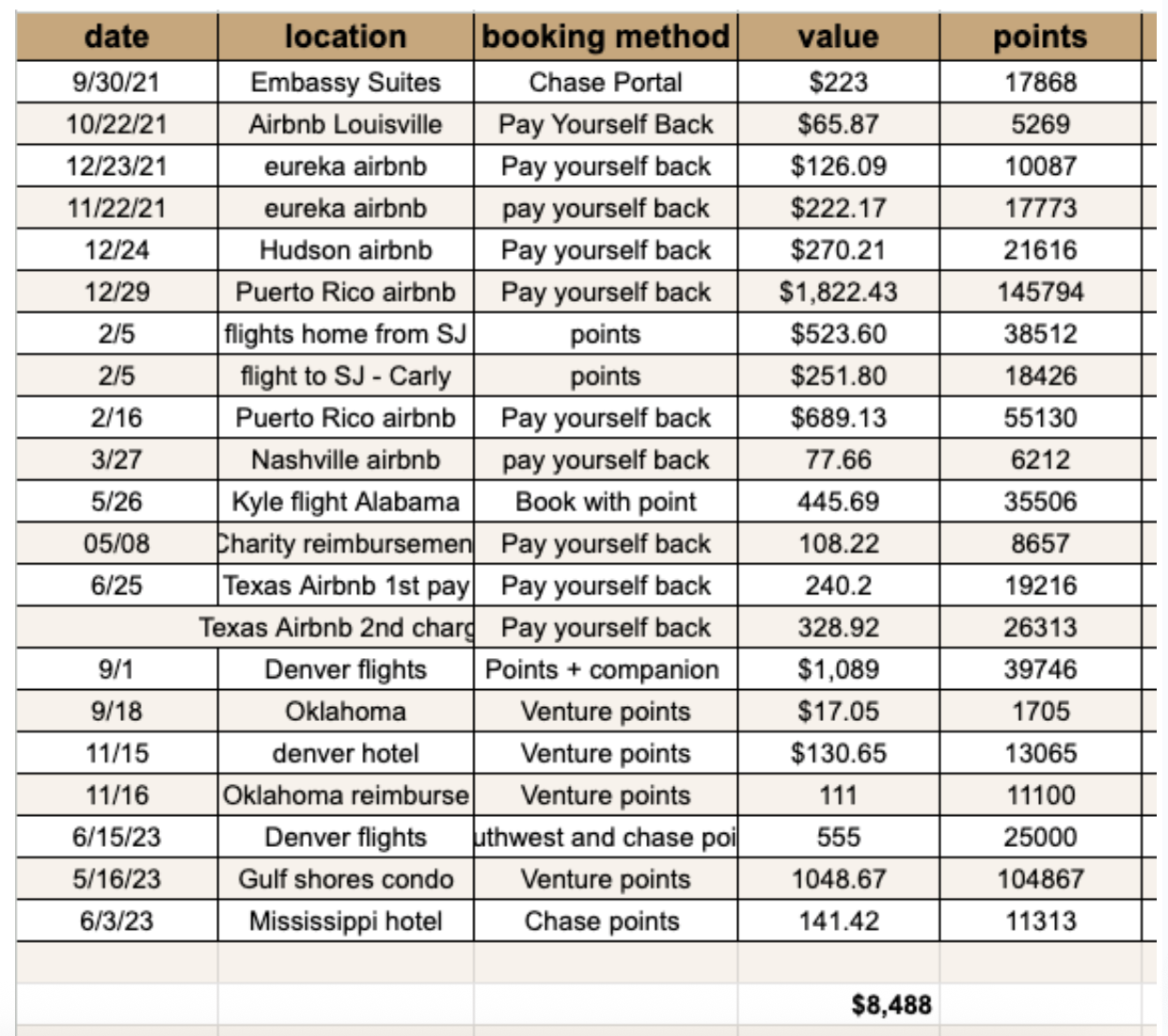

Trips I’ve Taken

I stopped tracking this in earnest several years ago (my bad!), but here’s my log of travel earned in the first 2 years of travel hacking. The value is how much I would've paid without points. I only included things on this list that I was able to fully cover.This is an average travel value of $404 per month - which is way more than I could ever earn simply trying to get 1-3% cashback on my daily spend. You simply don't "travel hack" with a credit card you keep open for years and use for shopping. You travel hack with referrals and sign on bonuses (remember, this is referrals between me and Kyle. Not because of Debt Free Mom.)

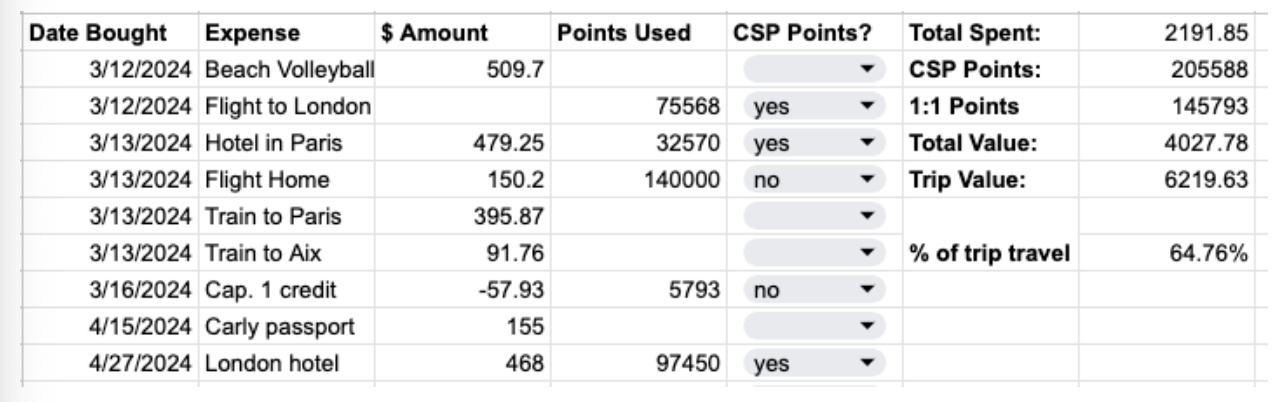

And this is our major 2024 travel hacking: our London/Paris Trip in Summer 2024 including the breakdown of what we paid vs. what we covered with travel rewards. CSP stands for Chase Sapphire Preferred. The 1:1 points are Capital One. What this chart is saying is that when it comes to the airfare, trains, and hotels, we would've spent $6,219 for this list on these dates, and instead we spent $2,191:

Final Thoughts and Mom Math

If you’re arriving at the end thinking “that’s complicated and risky!”, you’re right. The cautions and guardrails I asked myself before beginning are there for a reason. The time involved is more work than choosing not to travel hack.

Something complicated or risky does not always have to be avoided. Each person should answer for themselves if the benefits outweigh the risks - in each season of life, because the answer may change over time!

Start small, build up your experience over time, and always be willing to change your mind.

Mom Math #1 At BEST, the highest earning rate of anything I listed here is 6.25% (chase travel earns 5% and the points can be worth up to 25% more when redeemed for travel).

The interest rates on these cards currently run between 20-28%.

Remember the math: if you do NOT pay every purchase off in full every month (preferably every pay period!) then for every dollar you spend at best, you will earn 6.25 cents in rewards and be charged 28 cents in interest for every month that the dollar is not paid off.

I cannot emphasize this enough: if you do not have a clear track record of responsible credit card use in a way that adds to your financial health, do not be enticed by these rewards. The net effect will be backwards momentum if you earn the rewards then get slapped with a monthly interest charge.

If you're tempted to overspend and pay slowly, you are much better off paying for your expenses with a debit card and saving up cash for travel. That will have a higher net effect positive on your finances than earning rewards while paying interest.

Mom Math #2: Yes, annual fees are "annoying" (and get charged right away when you open the card!). But remember to ask yourself "what do I get in exchange for paying this fee?" If the sign on bonus is going to be worth $750 towards your next trip, would you pay someone $95 in exchange for a few nights in a hotel? You betcha! So think of the annual fee as the discounted price of the travel you later cash in on!

Mom Math #3: You can say "not right now" to this entire thing and nothing bad will happen. Remember my story at the top? I paid off all my debt, saved my full emergency fund, gave birth to all my babies, and bought my first home before I started using credit cards. If you have a relationship with debt that makes you hesitant to go down this path, don't go down this path! This may not be for you right now - maybe never. And good, amazing things can and will still come your way. At home exactly where you are. And in travels in the future! With or without credit cards.

If you're ready to go down this travel hacking path responsibly, the Care Creates Community is taking the month of May to focus on summer plans, travel, and travel hacking! I'll be going live in the community to answer Travel Hacking Q+As and would love to have you join us! It's only $9 per month, cancel anytime, and our topic changes every month!

join the Care Creates Community for only $9 and watch our Live Travel Hacking Q+A on Thursday, May 8th at 7:30pm CT.